While much of the nation continues to grapple with housing shortages and elevated home prices, Naples and Southwest Florida have experienced a more nuanced shift in the real estate market.

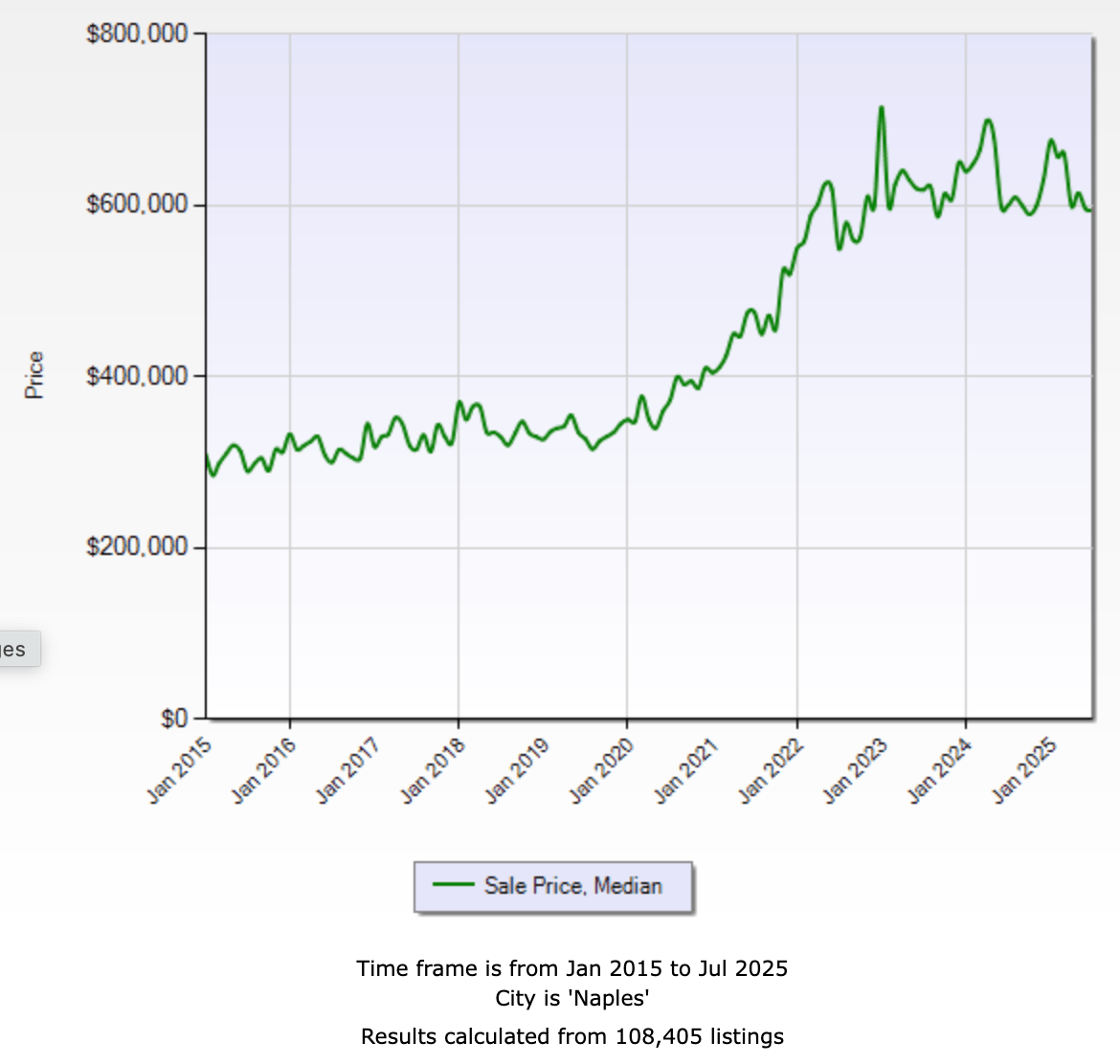

During the onset of COVID-19, Florida witnessed a historic influx of both investors and new residents. Investors were eager to capitalize on record-low interest rates, while many individuals from higher-tax states sought to relocate, motivated both by lifestyle changes and dissatisfaction with restrictive pandemic policies. The rise of remote work made such moves increasingly feasible, fueling unprecedented demand. In several Florida ZIP codes, home prices surged by as much as 80–100%.

This rapid appreciation continued until September 28, 2022, when Hurricane Ian—a Category 4 storm—devastated the region with storm surges of up to 20 inches, resulting in billions of dollars in damage and significant loss of life. Market confidence was further shaken by Hurricane Milton on October 5, 2024, a less destructive event but one that added psychological weight to an already fragile environment.

In the aftermath, skyrocketing insurance premiums and special assessments placed acute pressure on coastal properties, particularly high- and mid-rise condominiums, which have seen valuations fall by up to 30% from peak levels. Single-family homes proximate to the Gulf have declined 10–15%, while inland properties are down approximately 7–10%.

Yet despite these corrections, prices have stabilized—largely due to the phenomenon often referred to as the “golden handcuff.” Roughly 60% of U.S. homeowners currently hold mortgages below 4%, a historically low threshold. This dynamic has constrained inventory, as few owners are willing to forfeit such advantageous financing. Even investors who may not be meeting rental projections are under little financial strain with rates near 3%, further limiting distressed sales.

At present, I have 25 out-of-state buyers positioned on the sidelines, awaiting both lower rates and the possibility of additional price declines. However, it is my view that values are unlikely to erode meaningfully from current levels. Inflationary pressures accumulated over the past four years have created a pricing floor, and with economic conditions strengthening and interest rates expected to ease, we may be at a market inflection point.

For those waiting for further depreciation, the greater risk may be missing the bottom altogether.

For insight into opportunities in this evolving market, please feel free to contact:

Mike Kussmann

Alfred Robbins Realty Group